Let’s go skiing

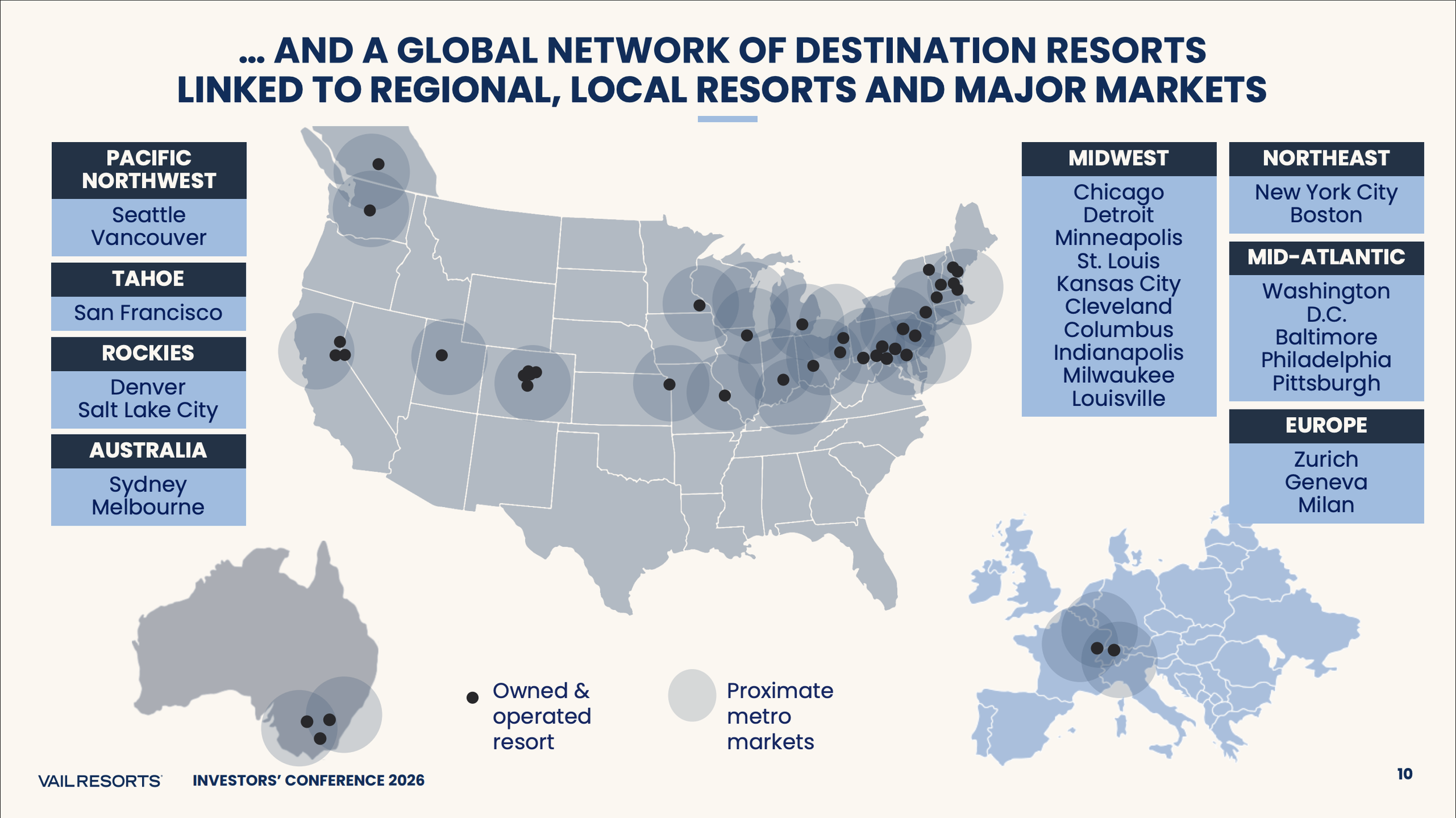

Vail Resorts (MTN) is a leading global operator of mountain resorts, owning and operating 42 ski areas across four countries. The company has over 2 million guests pre‑committed each season through its Epic Pass and other advance purchase products. This creates highly visible recurring revenue for the company. This network of strategically located destination resorts, paired with its subscription pass model creates a strong cash generating business. With only two owned resorts in Europe today, despite Europe being the world’s largest ski market, they still have a long runway for international expansion on the continent.

Vail Investors’ Conference 2026

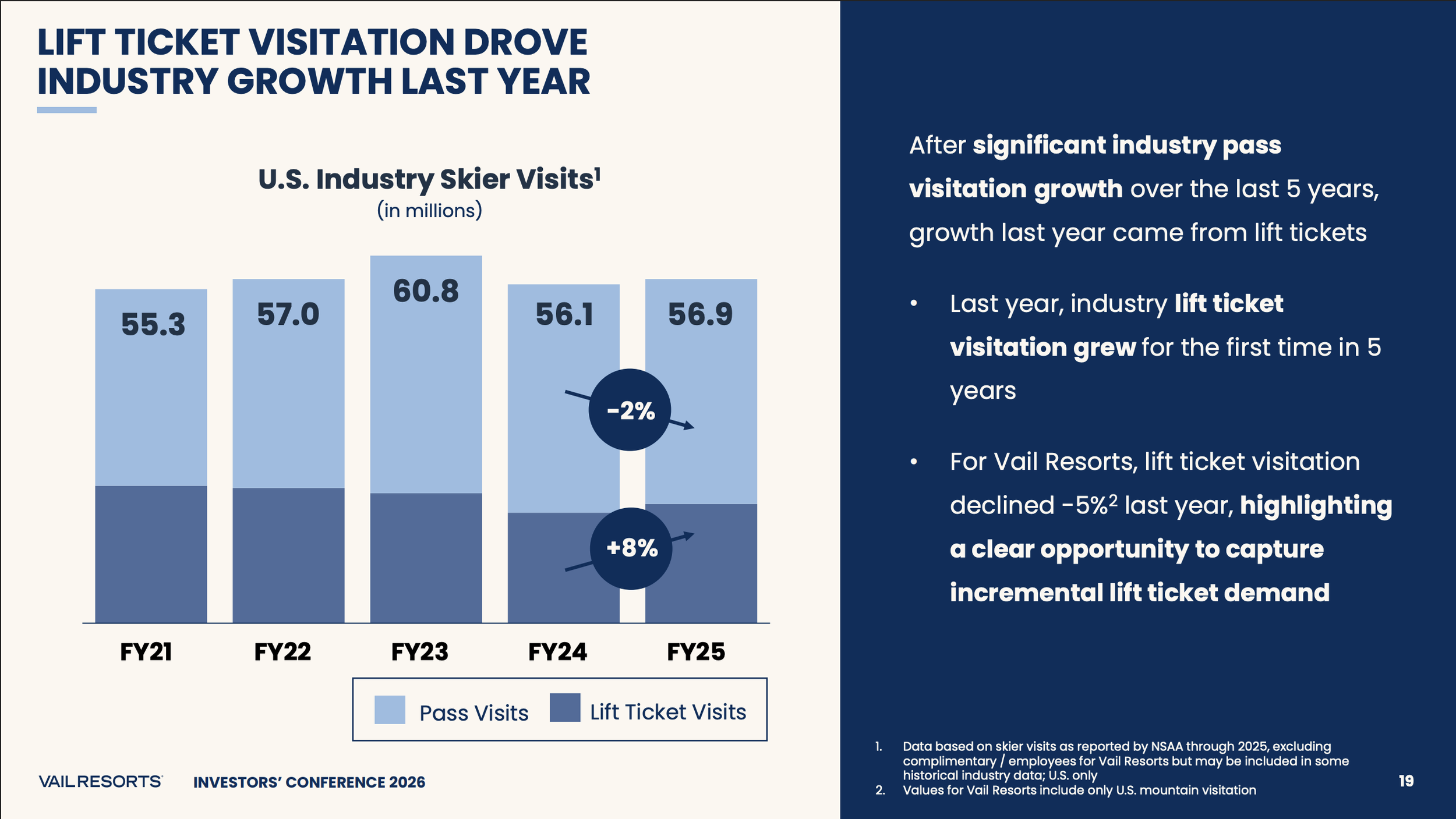

Over the last several seasons, winter conditions in the Rockies have been increasingly unreliable, with record‑low snow and unusually warm temperatures reducing terrain availability and shortening operating windows at key Colorado and Utah resorts. These conditions have driven meaningful declines in skier visits. Vail has recently reported mid‑teens to mid‑20% visitation drops at its Rocky Mountain resorts in poor seasons. This is putting pressure on lift, ski school, and on‑mountain ancillary revenue. On resort EBITDA margins have faced similar declines, despite some offset from pre‑sold Epic passes. Looking ahead, the current strong El Niño is expected to produce another warmer‑than‑average winter across much of the northern U.S., including the Rockies, suggesting another challenging year for volume recovery and creating continued downside risk to near‑term earnings and margin performance if snowfall once again tracks below historical norms.

Vail Investors’ Conference 2026

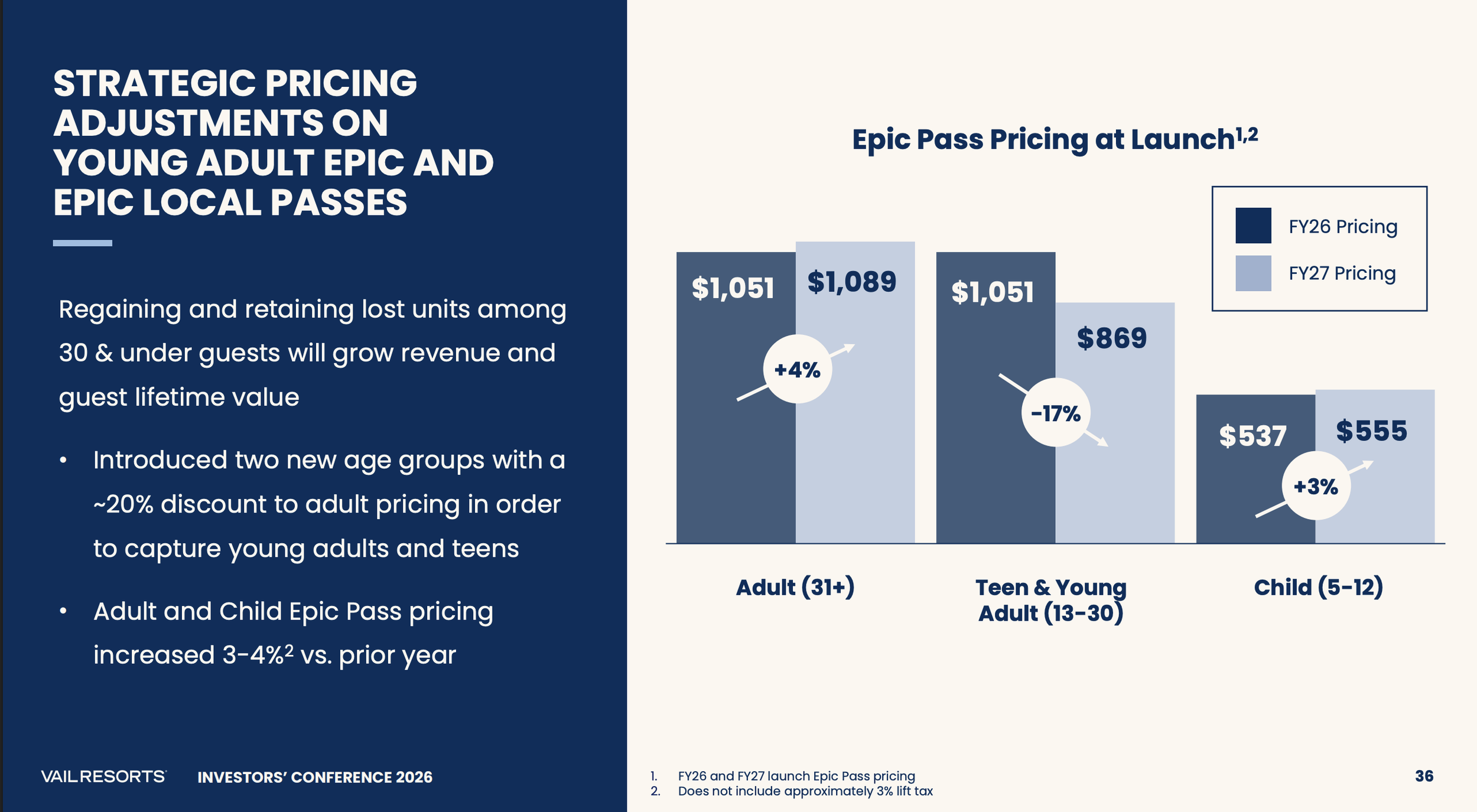

Vail continues to position itself at the premium end of the ski market, with the full‑access Epic Pass priced around $1,089 for adults ages 31 and older reinforcing the brand’s focus on higher‑income, destination‑oriented skiers. These price points sit squarely in the discretionary “luxury experience” bucket at a time when U.S. consumer sentiment has fallen back toward multi‑decade lows, prompting more caution around big‑ticket leisure spending and weighing on demand for high‑priced season passes and destination trips. In response, Vail has introduced new discounted Epic Pass tiers for teens and young adults ages 13–30 at roughly a 20 percent discount to the standard adult price (about $869 versus $1,089 on the 2026–27 offering), explicitly targeting younger skiers after management saw softer pass sales and weaker visitation among this cohort in the post‑Covid period.

Vail Investors’ Conference 2026

Vail Investors’ Conference 2026

After four challenging years marked by uneven snowfall, operational missteps, and deteriorating investor sentiment, Vail has moved to reset the narrative by bringing back long‑time former CEO Rob Katz, who resumed the role in May 2025 after previously leading the company from 2006 to 2021. During his prior tenure, Katz oversaw the launch of the Epic Pass, an aggressive resort acquisition strategy, and significant long‑term value creation for shareholders, with the stock compounding from the mid‑2000s to a record high near the mid‑$300s by late 2021. Today, shares trade around $135, more than 60 percent below those highs, suggesting that the market is already discounting a “worst‑case” combination of structurally weaker demand, persistent weather headwinds, and margin compression.

MPW Internal Estimates

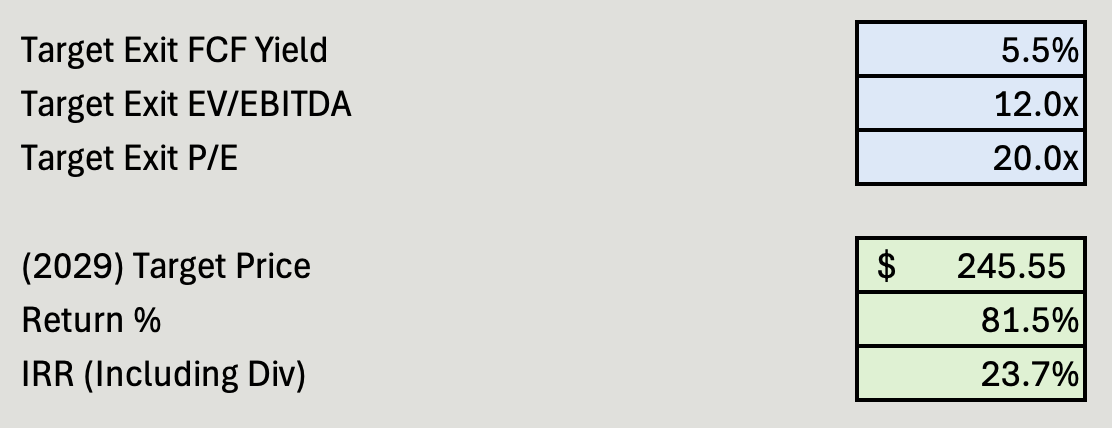

Importantly, Vail’s predominantly fixed‑cost model, encompassing lift infrastructure, snowmaking, leases, and corporate overhead, creates substantial operating leverage to skier visits and snowfall. A recovery in Western snow conditions and a normalization of visitation would allow a large portion of incremental revenue to fall through to EBITDA, driving outsized margin expansion and earnings growth. On our base‑case 2029 earnings forecast, applying a 20x exit P/E multiple implies a potential value of roughly ~$255 dollars per share, still below the peak multiples the stock has historically commanded in stronger cycles. We set our 2029 price target modestly lower at $245 to reflect execution and weather risk, which represents approximately 80 percent capital appreciation from the opening price of $135.27 on June 8, 2026; including Vail’s dividend, this equates to an expected internal rate of return (IRR) in excess of +20% over the period.

As of mid-day 6/8/2026. Performance data may be inaccurate, do not rely on it for investment decisions.

Disclaimer

This article is for informational and educational purposes only and does not constitute investment advice or a recommendation to buy or sell any security. Readers should conduct their own research and consult with a qualified financial advisor before making any investment decisions. The author and publisher disclaim any liability for any losses or damages incurred as a result of reliance on the information provided herein.

Citations

MPW Internal Estimates